Daily market review Nov 7 (Cap-weighted indices outperform Equal-weighted indices)

Daily market review Nov 7 (Cap-weighted indices outperform Equal-weighted indices)

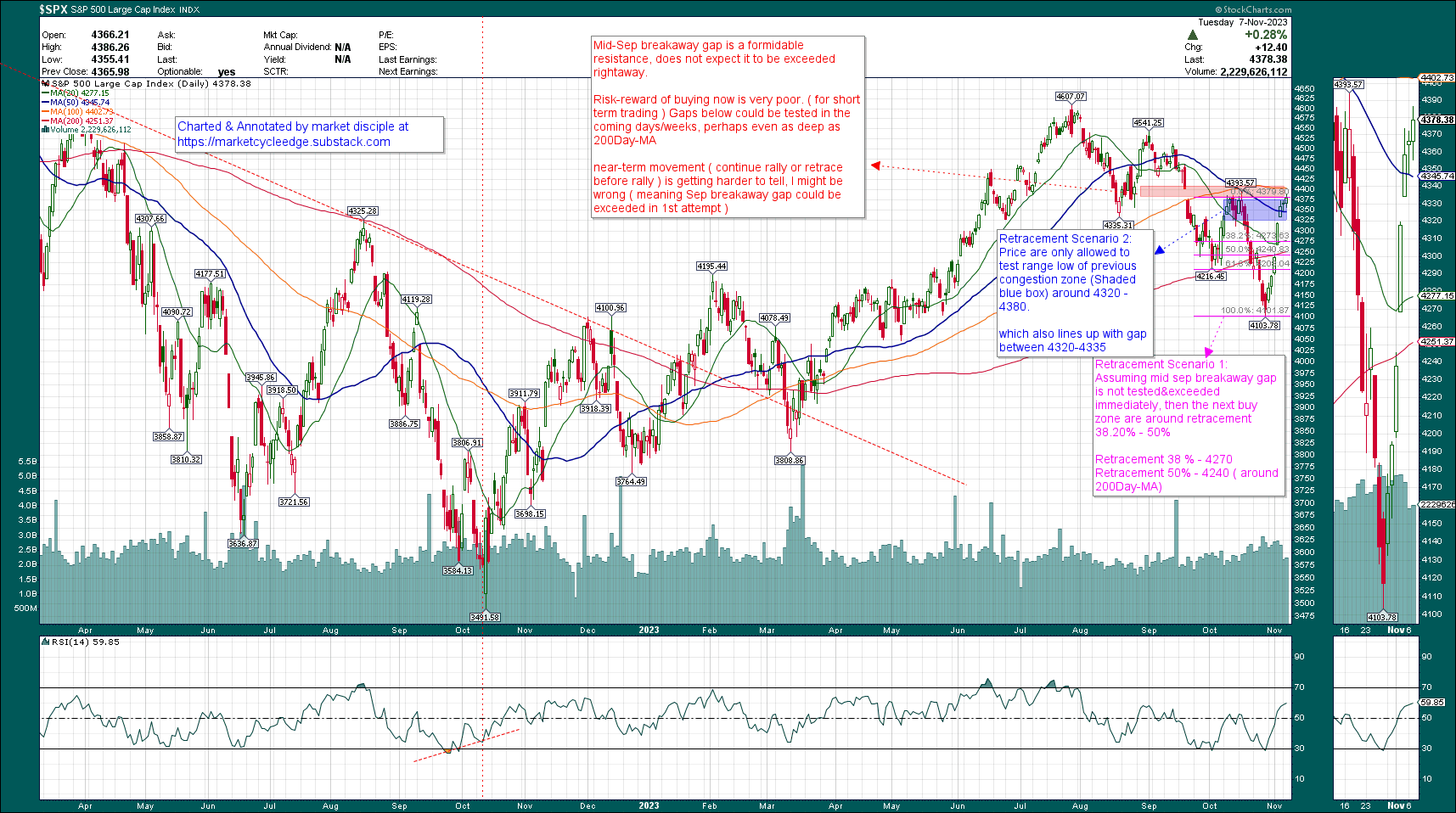

Overview of S&P 500

I still think the Mid Sep Breakaway gap is a formidable resistance, does not expect it to be tested&exceeded immediately. Dips in the coming days are buyable. There are 2 retracement scenarios, ( both are equally likely ), stated and illustrated inside the chart.

It’s possible that I might be wrong about Sep breakaway gap not being exceeded in 1st try, predicting near term movement is getting harder, because of the following 2 reasons,

Reason 1: Some big institutions haven’t got in on the rally/are still under-allocating equity, if this scenario is true, they might not wait for pull back and will keep chasing the rally instead. ( pull back might still come at a later stage to shakeout some weak hand )

Reason 2 : pull back/retest of previous support might only happen to the equal-weighted indices, Mid&small cap, but not Cap-weighted indices at the moment ( since cap weighted indices are stronger performer than Mid&Smallcap, equal-weighted counterpart)

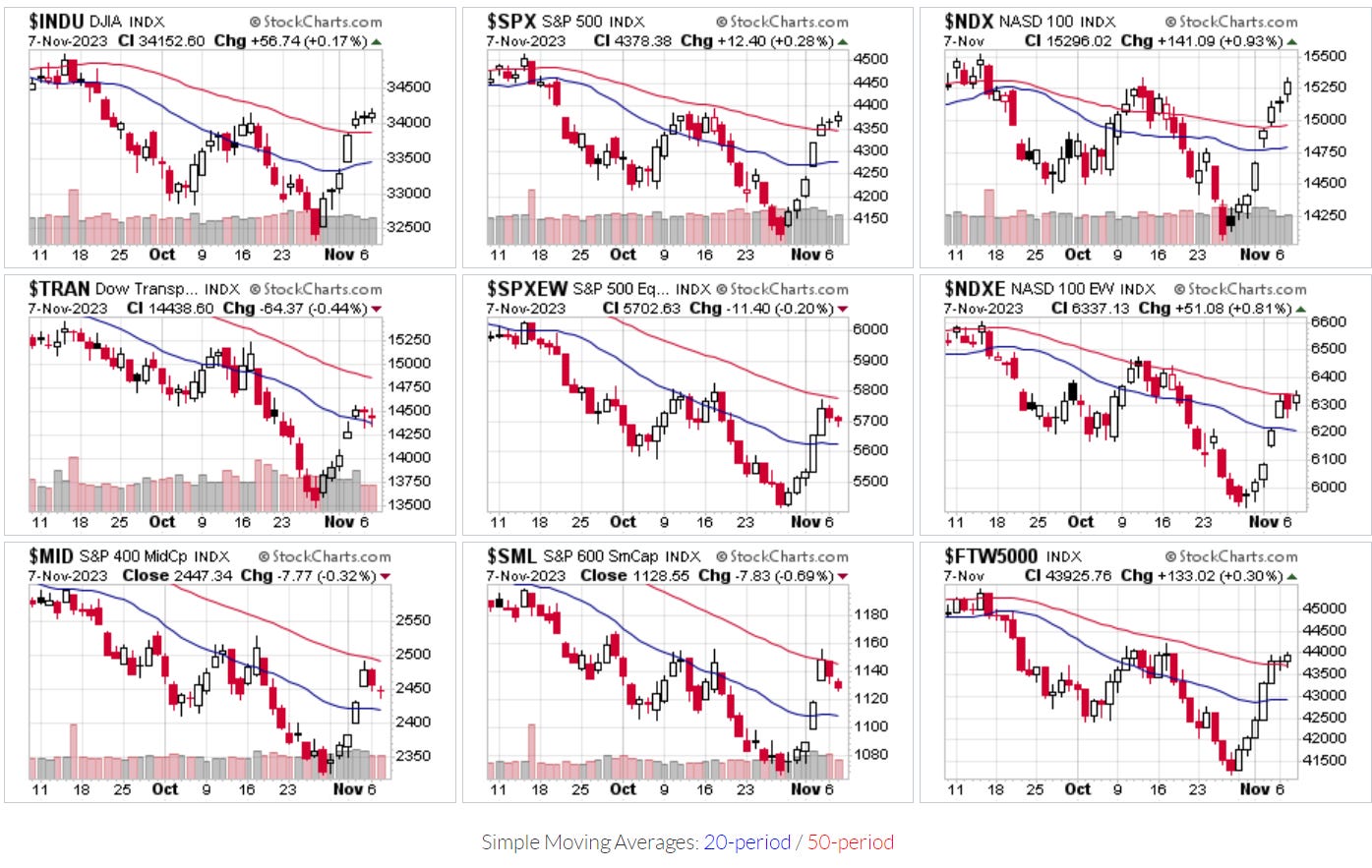

Broad market overview

Equal-weighted indices, Mid&Small cap are underperforming Cap-weighted counterpart for 2nd day in a row.

Bullish rally sustainable conditions assessment

MOVE index

MOVE close around 120, would like to see it closing below 120 consistently and move closer to 100 in the coming days.

Relative strength of Equal-weighted SPX vs Cap-weighted SPX

Need a few more days to get initial assessment

Consumer discretionary vs Consumer staples on Equal-weighted basis

Need 1- 2 months to get initial assessment

Transportation

Will be monitoring in the coming days to see when price can recapture 200day-MA and previous swing high at 15250

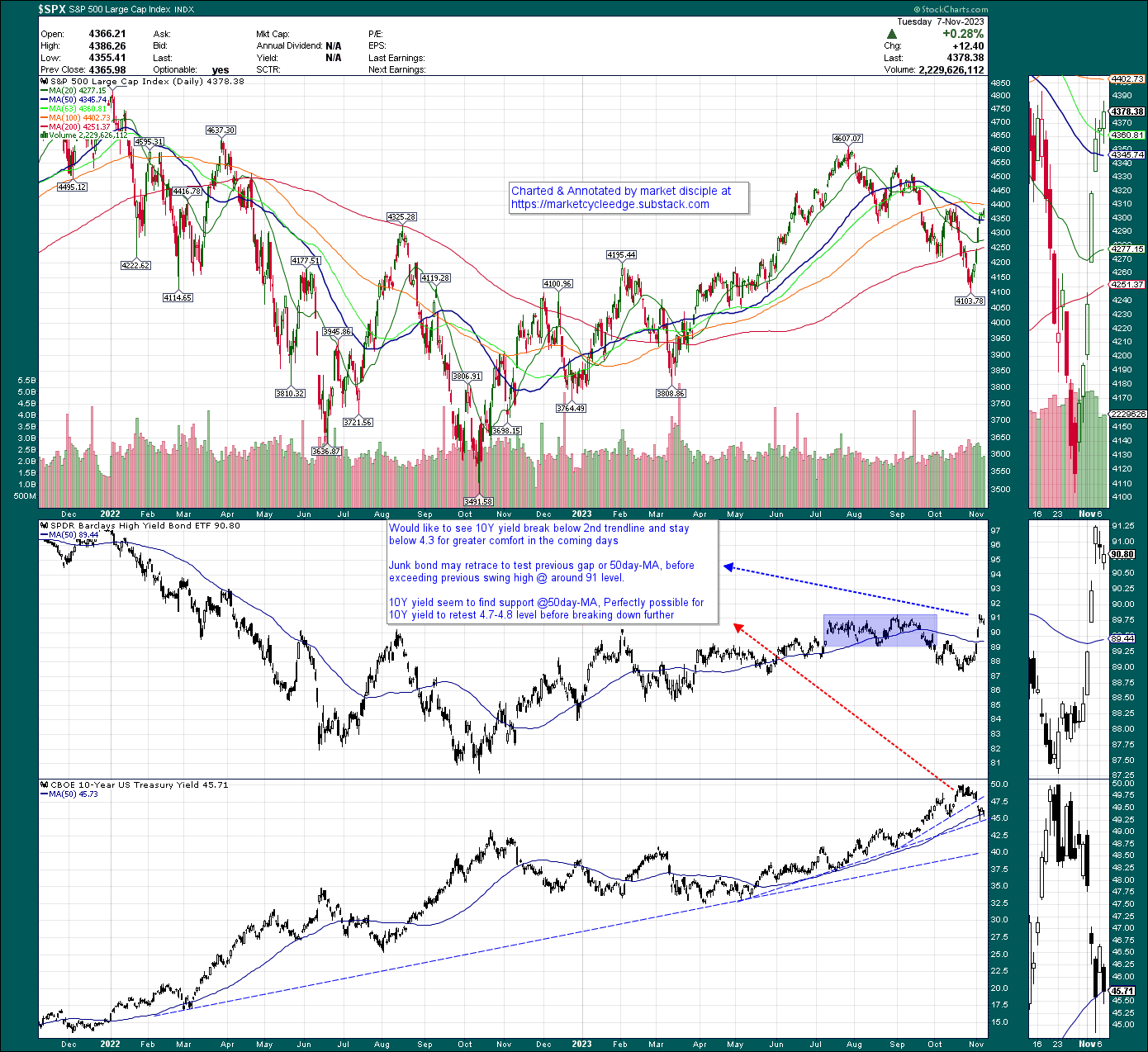

10Year Yield (TNX)

10Y yield seem to find support @50day-MA, Perfectly possible for 10Y yield to retest 4.7-4.8 level before breaking down further

Junk bond may retrace to test previous gap or 50day-MA, before exceeding previous swing high @ around 91 level.

Dollar index (DXY)

DXY retested&closed at 105.50 level. Need to see it resuming breakdown, and break below 200day-MA 103 level in the days ahead

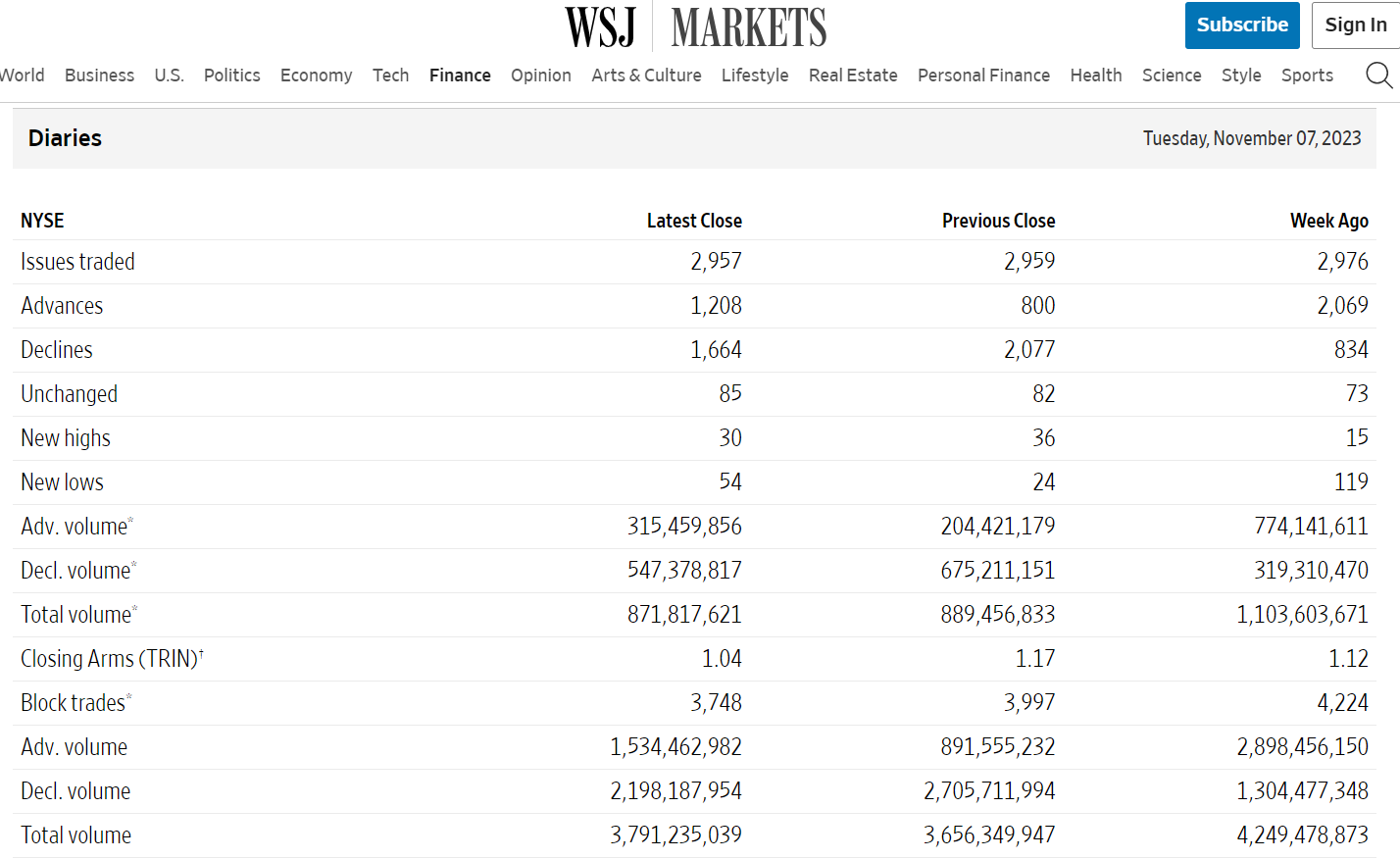

NYSE AD ratio and volume statistics

Monday Nov 6, 2.58 to 1 NYSE Decliner to advancer ratio (2077/800)

Tuesday Nov 7, 1.38 to 1 NYSE Decliner to advancer ratio (1664/1208)

Tuesday underlying breadth is better than Monday.

% of SPX stock above 50days and 200 days MA

Market breadth is improving,

percentage of SPX-Stock above 50days-MA, recover from Oct-27 low of 10.6 to 45.2% .

percentage of SPX-Stock above 200days-MA, recover from Oct-27 low of 24.6 to 40.2% .

Sector performance

Offensive sector ( Technologies, Communications , Consumer discretionary) outperform Defensive sector (Utilities, consumer staples) from Nov 1 – 7. Financials are rank no.4, that’s a very welcome development.

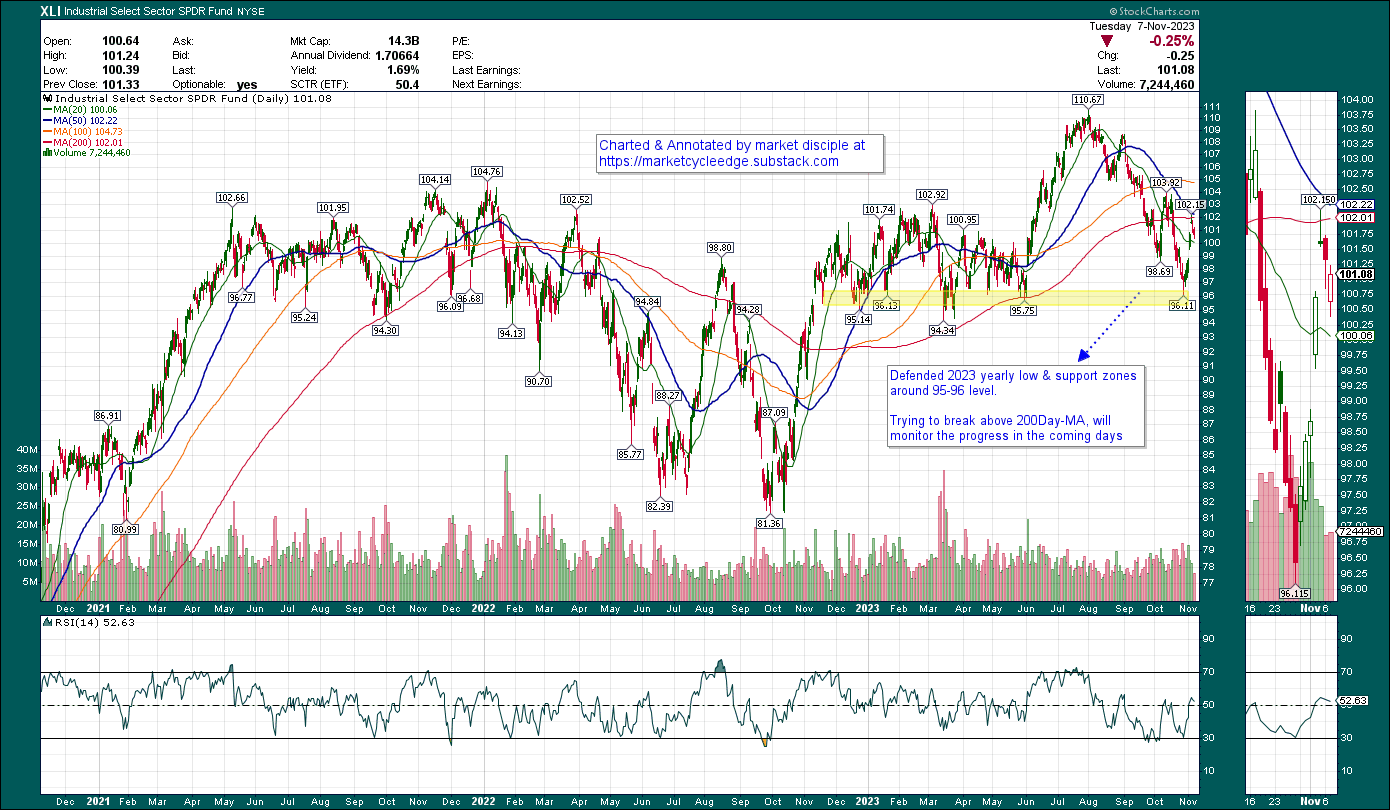

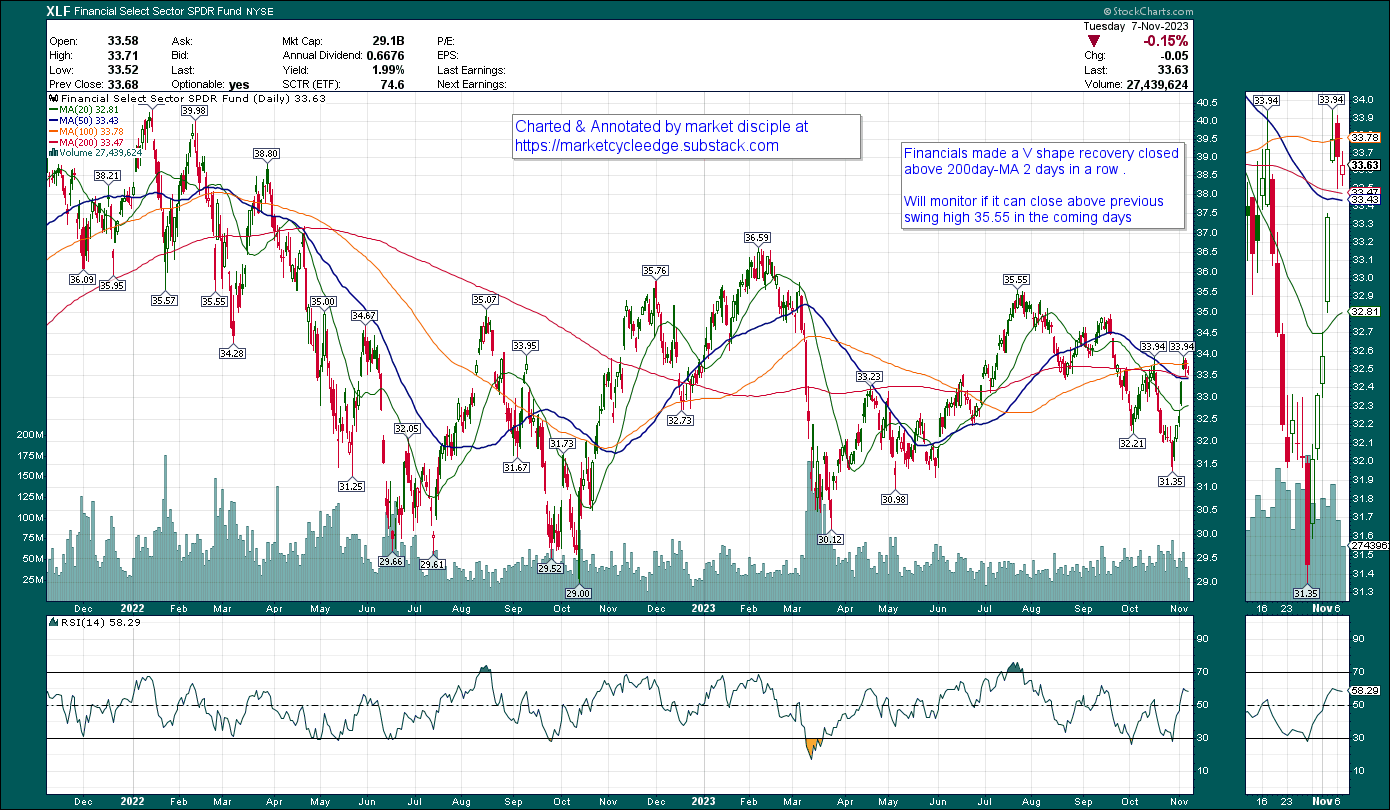

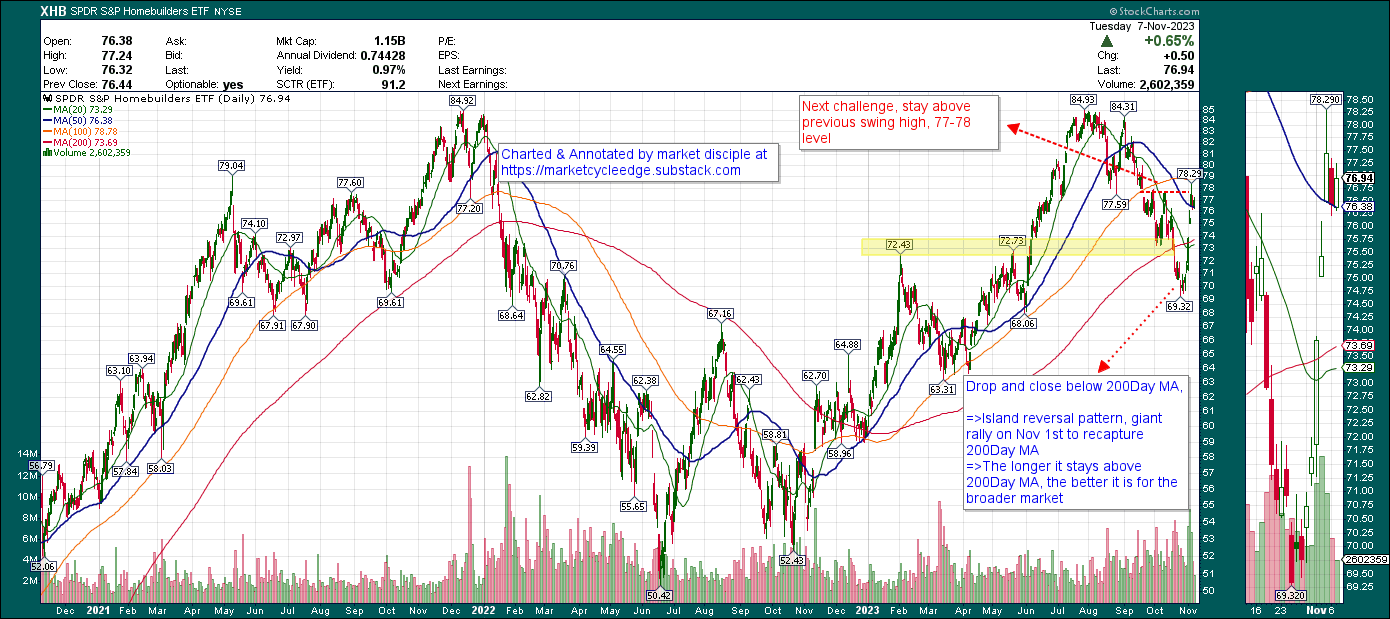

For market rally to be sustainable, the broader market need to step up , let’s look at industrials, financials and homebuilder ETF (XHB)

Industrials

V shape recovery is ongoing, and will monitor when it can close above 200Day-MA.

Financials

V shape recovery has propelled it to close above 200day-MA for 3 days in a row. The longer it stays above 200day-MA, the better it is.

Homebuilder ETF

Still waiting for it to breakup above previous swing high at 77-78

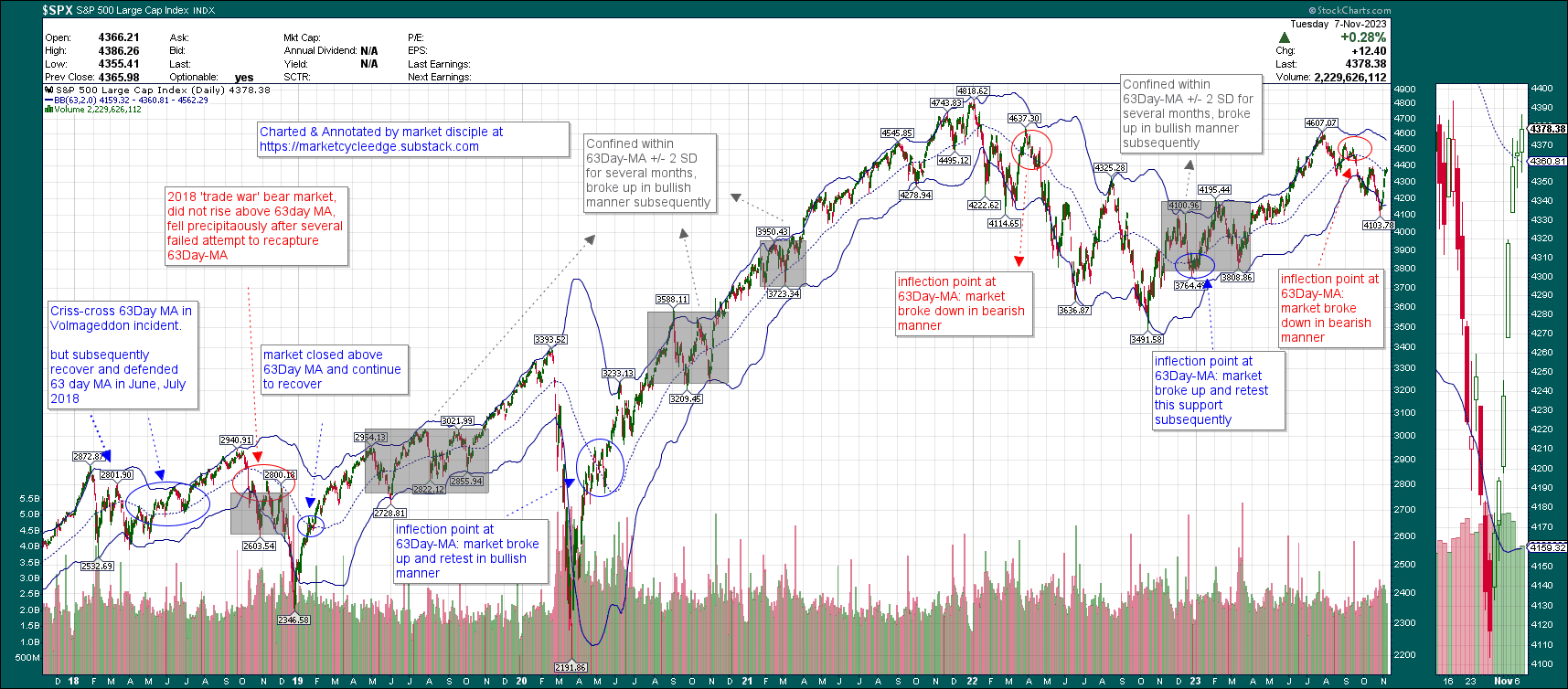

Bollinger band model ( 63day-MA + 2SD band.)

Rationale for this model are explained in previous blog entry if new readers would like to know more.

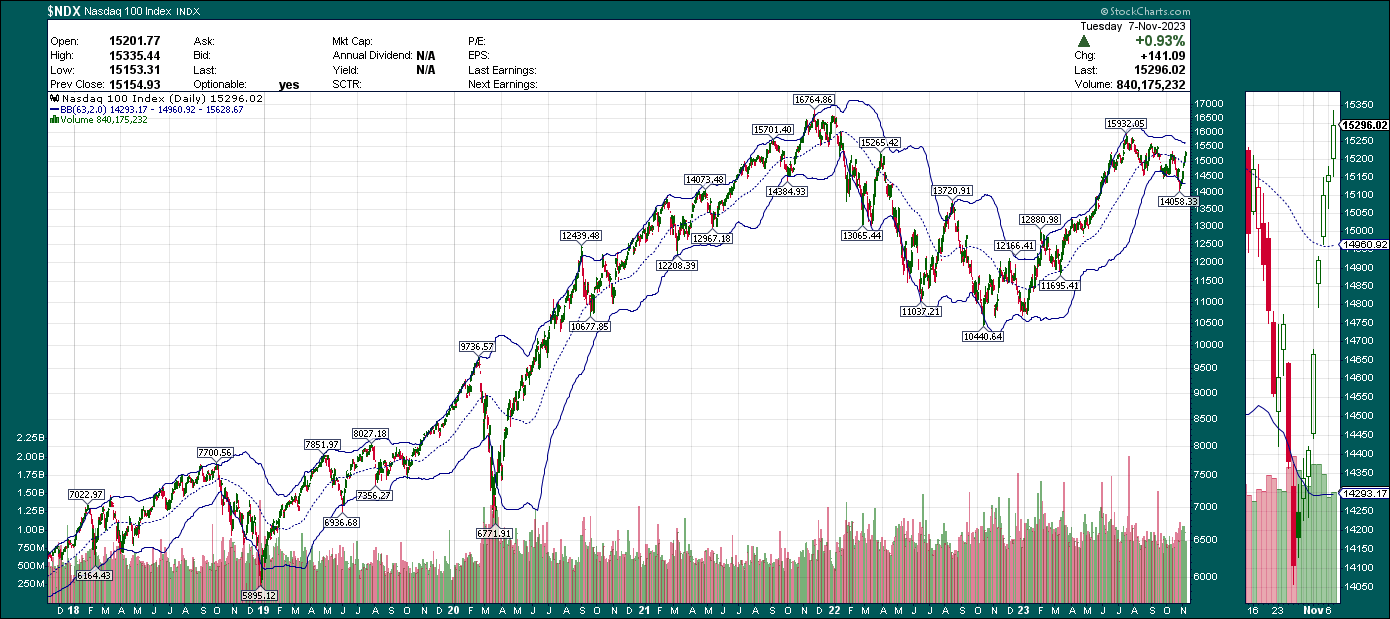

Let look at SPX and NDX using this model,

SPX stay above 63day -MA for 2 days in a row

NDX stay above 63day-MA for 3 days in a row

As always, we will continue to monitor the charts, assess the bullish/bearish evidence day-by-day to make appropriate capital allocation and investment decisions.

Disclaimer : The information presented here are for research and education purpose only, and does not constitute investment advice, trading recommendation, author shall not liable for any action taken by any individual/company with regards to the information presented here or any part of the website - https://marketcycleedge.substack.com/